Do you feel your credit stands in the way of getting approved for financing for a home or a new car? Having bad credit can do more than prevent you from getting approved for a loan; you may also have to pay more for insurance and provide a security deposit on utilities if you move. Financial challenges can occur to anyone, any time. The good news is you can begin to improve your credit immediately. While repairing your credit does take time, it’s possible to improve it as long as you’re dedicated to positive financial habits.

Do you feel your credit stands in the way of getting approved for financing for a home or a new car? Having bad credit can do more than prevent you from getting approved for a loan; you may also have to pay more for insurance and provide a security deposit on utilities if you move. Financial challenges can occur to anyone, any time. The good news is you can begin to improve your credit immediately. While repairing your credit does take time, it’s possible to improve it as long as you’re dedicated to positive financial habits.1. Pay Your Bills On Time

This is one of the easiest ways to build your credit score and, most importantly, build great financial habits. When you pay your bills on time, you ensure no payments end up in collections.

• Create a budget

A budget tells you where your money is going and helps you plan to spend it wisely. Start by calculating how much income you have each month, from work, child support, etcetera then, tally up your expenses, from ones that are due monthly, such as utilities and rent or a mortgage, to those due less often, such as taxes, car maintenance, etc. Also, be sure to include other expenses such as coffee runs, lunches with coworkers and other non- essential expenses. This will give you a clear picture of your financial state and help you see where you can save money.

• Reduce non-essential expenses

The first place to make cuts if you’re trying to save money is your non-essential expenses. Try making coffee at home or at work instead of buying one every morning, and reserve going out to lunch for Fridays to save on restaurant expenses. While it may not seem like much, making small cuts will help you save money, pay down debt and live well within your means.

• Track your spending

Creating a budget is only half the battle; the other half is tracking your expenses. Tracking helps you stick to your budget. Write your expenses in a notebook or input them in an app; either way, take the time to track your spending and you’ll always know where your money is going.

• Get current on accounts that are past due, but not charged off

Contact your creditor to find out how to get current on the account. If you pay your debt in full, the balance will become zero and the account will be paid off. However, it may stay on your report for seven years after the date of charge off.

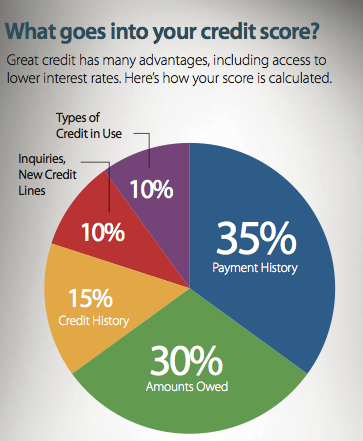

2. Review Your Credit Score and History

The place to begin when improving your credit is with your credit history. You’re legally entitled to a free credit report from each of the credit bureaus - Equifax Canada and TransUnion Canada - as long as you request your free copy. Reviewing your credit periodically allows you to see if there is information that may negatively impact your score.

• Look for incorrect information such as payments that were incorrectly reported late, accounts that aren’t yours, etcetera

• Be aware of accounts that are past due, that are late, have been charged off (i.e., the payment is 180 days past due) or have been sent to collections, as well as accounts that are over the credit limit

• Dispute inaccurate or incomplete information

While you can do this online or over the phone, it may be best to do it through the mail so you can create a paper trail. If your dispute is legitimate, the credit bureau will investigate and give you a response.

3. Pay Down Your Debts

If you have debt, try to pay it off. If that’s not possible, pay it down to as low as you can.

• Reduce your debt-to-income ratio

When assessing your loan application, lenders consider your debt-to- income ratio; that is how much debt you have compared to your income. The lower your ratio, the more likely you’ll qualify for a great loan. Start with the cards or debt with the highest interest rates first and, once you’ve paid them off, go to the debt with the next highest interest rate. Over time, you’ll have paid off your debts.

• Increase your available credit

You may be able to increase your credit limits on your credit cards if you’ve been a good customer. Call your credit card company to learn more.

4. Use Credit Wisely

Once you have credit, it’s important to use it responsibly. Here’s how:

• Don’t open new accounts, unless you have to

Opening several new accounts at a time may raise red flags for potential lenders.

• Keep a low balance on credit cards and revolving credit

• Pay off debt instead of moving it to another account or to a new account

5. Seek Professional Help

If you have trouble making ends meet, notify your creditors and see a credit counsellor.

///...CP